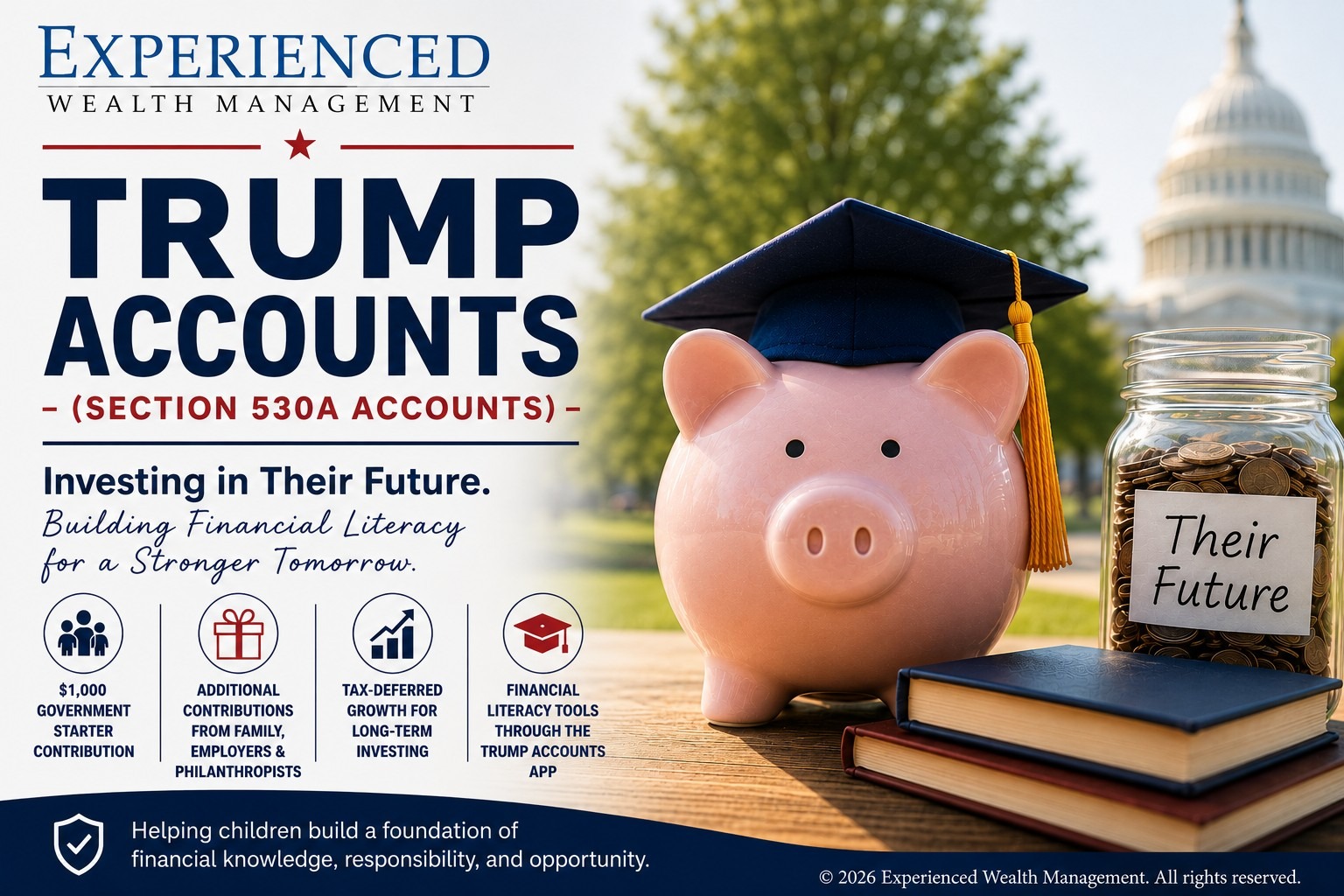

"Trump Accounts (530A Accounts)"

"Trump Accounts (530A Accounts): A New Way to Introduce Children to Investing and Financial Literacy".

One of the newer financial planning topics generating attention is the introduction of Trump Accounts for children. At first, I wasn't particularly excited about them. From a financial planning perspective, the accounts function much like a traditional IRA. Contributions are made with after-tax dollars, growth is tax-deferred, and withdrawals are generally taxed as ordinary income later. Because of that, I initially felt there were often better options available for many families, such as Roth IRAs (when eligible) or 529 plans.

However, after learning more about the program, my opinion has changed.

Trump Accounts are designed to help introduce investing and financial education to the next generation. Eligible children born between 2025 and 2028 can receive a $1,000 government-funded contribution, and parents, grandparents, family members, employers, and even charitable organizations may be able to make additional contributions. Current rules generally allow up to $5,000 per year in private contributions, while certain nonprofit and philanthropic contributions may not be subject to the same annual limits.

What I find most interesting is the growing involvement of philanthropists and businesses. Several large organizations and donors have already announced plans to help fund accounts for children, particularly those from lower-income families. This has the potential to introduce millions of young Americans to saving, investing, and long-term financial planning much earlier in life.

The other feature that changed my thinking is the educational component. The new Trump Accounts app is designed not only to track investments but also to help teach financial literacy and ownership. If used correctly, it could help a generation of young people better understand investing, compounding, and long-term wealth building.

Whether these accounts ultimately become a major planning tool remains to be seen. But anything that encourages financial education, investing, and personal responsibility at an early age is worth paying attention to.

As a financial advisor, I will be watching closely to see how families, employers, and philanthropic organizations use these accounts over the coming years.

Trump Accounts offer tax deferred growth on earnings and provide tax free withdrawals when distributions are qualified. Contributions may include after tax family contributions, pre tax employer contributions, and a one time $1,000 federal contribution for eligible children born between 2025 and 2028. Withdrawals prior to age 59½ may result in a 10% IRS penalty tax, in addition to current income tax, and may be restricted until the child reaches age 18. Annual contribution limits and other restrictions apply. Some Trump Account rules and regulations are still forthcoming from the U.S. Treasury and IRS. Clients should consult with a qualified tax advisor or financial professional before making any decisions.